To:

Insurance Underwriting and Claims Executives

Business Development and Loss Prevention Team Leaders

From: Peter M. Wells Business Group (PMWBG)

Re:

Insurance Technology Update – Building Component Failure Predictive Solution

Top 4 U.S. Homeowners Writer Verifies Efficacy of Life Cycle Cost (LCC) Predictive Scores Carrier Reports Program Highly Predictive of Residential Loss Concerns / Adding Lift.

Open the following link to view this Bulletin:

Discussion:

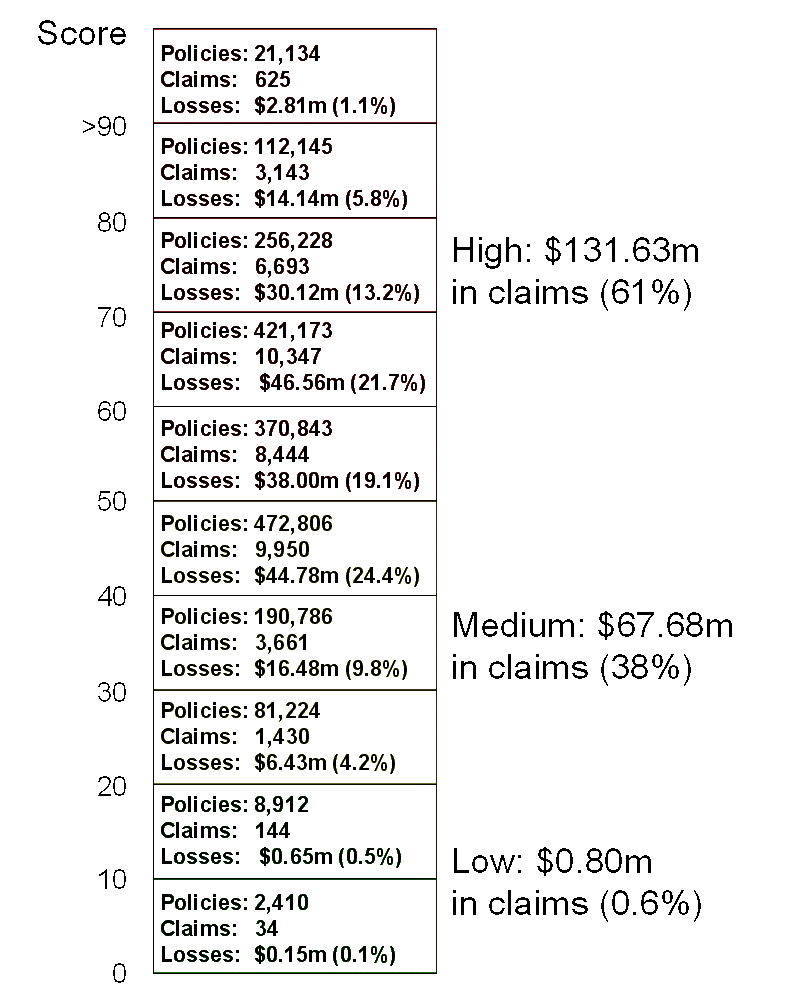

With nearly 27 million residential property records having now been studied from five top homeowners insurance writers, and with a new, comprehensive multi-year analysis performed by a top 4 U.S. carrier, results demonstrate that Life-cycle Cost (LCC) Data and Analytics from Peter M Wells Business Group is highly predictive of property claims from component failure and should become an actionable new variable in loss prevention, sales positioning and overall competitive pricing models for U.S. property writers. The impact is projected to be as much as $11 billion in loss savings for the homeowners’ side of the P&C marketplace, with at least $5 billion in premium lift annually. Success is derived from knowing in advance which major systems in homes will fail in the coming policy cycle so action can be taken on a risk specific basis.

| Bob Caramanno, Executive Vice President for the Wells Group, explains that LCC technology has uncovered the causes for a major component of all the losses insurers face – component failure. The LCC program was conceived by industry expert Peter M. Wells in collaboration with Whitestone Research of Santa Barbara, CA. and uses independent construction system research to evaluate the component parts of homes to understand component life-cycle. Tested on tens of millions of homes, this simple to learn and use web-enabled system uses sophisticated construction models to define the features of homes then looks to see how key components that drive insurance claims mature and fail. Using over 22,000 components of life-cycle trends that align with perils insured life-cycle is projected as homes mature based on simple to understand scores and associated reports. A score is affixed to each property each year with detailed back up available on line instantly to explain each score.

Whitestone is a firm that already delivers a similar solution for budgeting and predictive insights in the commercial facilities and home construction industry worldwide. The Well Group saw the possibilities for the insurance market and helped deliver a proven solution for new competitive advantage for insurance companies. |

|

Analysis shows that as many as 90% of the homeowners property claims insurers pay are now able to be forecasted for life-cycle exposure using the LCC scoring system with details on what will mature and fail annually in each home. Because of the extreme detail in LCC models, LCC data is effective writing new policies, but has a major impact when run against existing business that never had this kind of analytics review before. Other advantages carriers find include . . .

|

Age Scores Carriers Build Themselves

|

Industry findings show LCC reliably predicts loss experience offering a substitute to less property specific programs. |

|||||||||

LCC SCORES

|

|

|||||||||

For more information, contact:

Peter M Wells Business Group

262-347-6091

petermwells@peterwells.us